Company Archive

Singapore’s gaming-to-shopping company Sea to develop more games, financial services to strengthen internet ecosystem in Southeast Asia

Catherine Garcia

Comments off

The company, which is one of Southeast Asia’s biggest gaming firms, has traditionally published game titles in the region on its Garena

American Airlines flights resume after company experiences brief nationwide outage

Loknath Das

Comments off

An American Airlines Boeing 737 passenger plane taxis from a gate to the runway at Ronald Reagan Washington National Airport in Washington,

Honor 8 Will Not Get Android Oreo-Based EMUI 8.0 Update, Confirms Company

Loknath Das

Comments off

Honor has confirmed that the Android Oreo update will not be coming to the Honor 8 smartphone. The company confirmed the information on Monday via

Apple Is No Longer America’s Favorite Tech Company

Loknath Das

Comments off

As the reality distortion field around Apple has faded in the past few years, people are becoming significantly less enamored with the company than

HTC Said to Be Exploring Strategic Options, Including VR Business Spin-Off and Company Sale

Loknath Das

Comments off

Smartphone maker HTC Corp is exploring options that could range from spinning off its virtual reality (VR) business to selling itself, Bloomberg reported on

Apple on Track to Become First Trillion-Dollar Company

Loknath Das

Comments off

Apple Inc AAPL 161.06 +0.61% Apple Inc. (AAPL Apple Inc AAPL 161.06 +0.61% ) is on track to become the first trillion-dollar

How Apple could become a $1 trillion company

Loknath Das

Comments off

Apple reported its earnings this week, and with a surprisingly positive report the shares spiked again as Apple signaled a potential huge

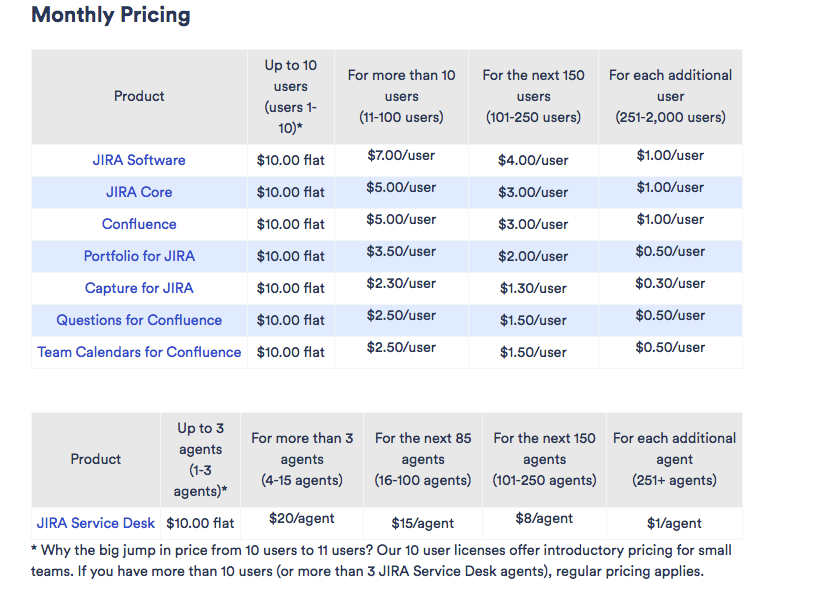

Your Company May Soon Pay More for This Key Software

Loknath Das

Comments off

Many Fortune 500 companies will probably pay more to use Atlassian software starting next month, but it’s sort of hard to tell given the